Weekly Outlook

What Happened This Week?

- Canada's annual inflation rate fell to 1.7% in July, a decrease from the 1.9% increase recorded in June, which supports another interest cut.

- The Reserve Bank of New Zealand (RBNZ) cut its Official Cash Rate by 0.25 percentage points to 3%. The central bank pointed to several factors for the move, including easing medium-term inflation pressures, a slow economic recovery, and uncertainty surrounding the impact of U.S. tariffs.

- U.K. inflation reached an 18-month high in July, rising to 3.8% from 3.6% in June. This increase, largely driven by a record jump in airfares, will likely prevent the Bank of England from cutting interest rates again soon.

- U.K. consumer confidence improved in August, rising two points to minus 17, as the Bank of England's rate cut to 4% boosted sentiment. However, lingering fears over inflation and unemployment mean consumers are still cautious.

- Sweden's central bank held its benchmark interest rate at 2%, but stated that it could cut rates again this year. This comes as annual inflation rose to 3% in July, exceeding the bank's target for a second consecutive month.

- Bank Indonesia has cut its benchmark rate for the second consecutive time, lowering the seven-day reverse repo rate by 25 basis points to 5.00% to support economic growth.

- The Fed's July minutes showed that most officials supported holding interest rates steady, but internal divisions are growing ahead of the September meeting. Cleveland Fed's Hammack opposes cuts due to rising inflation, while Boston Fed's Collins is open to them, citing concerns about the labor market.

- President Trump is reportedly considering firing Lisa Cook, a Federal Reserve governor appointed by President Biden, if she doesn't resign. This follows a mortgage fraud accusation from a White House housing official and is seen as the latest escalation in the White House's attacks on the Fed.

- U.S. existing home sales surprisingly picked up in July, rising 2% month-over-month to an annualized rate of 4.01 million. With prices also easing, this unexpected activity has raised hopes that the housing market could gain more momentum as it heads into the fall.

- According to a Conference Board survey, more U.S. employers are planning to slow their hiring in the latter half of 2025. The survey found that 20% of companies will reduce their hiring pace, nearly double the percentage that had similar plans a year ago.

- New filings for U.S. jobless claims increased to 235,000 in the week ending August 16, up from 224,000 a week earlier. This rise comes after the unemployed population hit a recent high earlier in the month.

- Following its August 7th decision to cut its key rate by a quarter-point to 7.75%, the Bank of Mexico's meeting minutes indicate that the central bank will likely continue to lower rates. However, the minutes also show that some board members are now leaning toward a more data-driven approach for future cuts.

- Consumer inflation in Japan, excluding volatile fresh food prices, stayed significantly above the Bank of Japan's 2% target. The index rose 3.1% from a year earlier last month, a modest slowdown from the 3.3% increase recorded in June.

- Japanese exports decreased by 2.6% year-over-year in July, marking the third consecutive monthly decline. This drop was a steeper fall than the 0.5% decrease recorded in June.

- Despite the drag from U.S. tariffs, European business activity remains resilient, according to recent PMI surveys. Activity slightly improved in Germany, continued to weaken but at a slower rate in France, and surged in the U.K.to a one-year high.

- Surveys indicate that business activity expanded in other major economies around the world. India's growth accelerated at its fastest pace in two decades, while both Australia and Japan also saw their rates of business activity increase.

- In August, U.S. business activity saw its strongest growth of 2025, with expansion across both the manufacturing and service sectors. The manufacturing sector's activity reached a new 39-month high, while the service sector continued to grow, but at a rate just below that of the previous month.

This Week’s Market Movers

Forex

- The EUR/USD is down after 2 weeks up.

- The USD/CAD is up for the 2nd week in a row.

- The NZD/USD is down more than 1.70%.

- The EUR/GBP is up after 3 weeks down.

- The AUD/USD is down more than 1.10%.

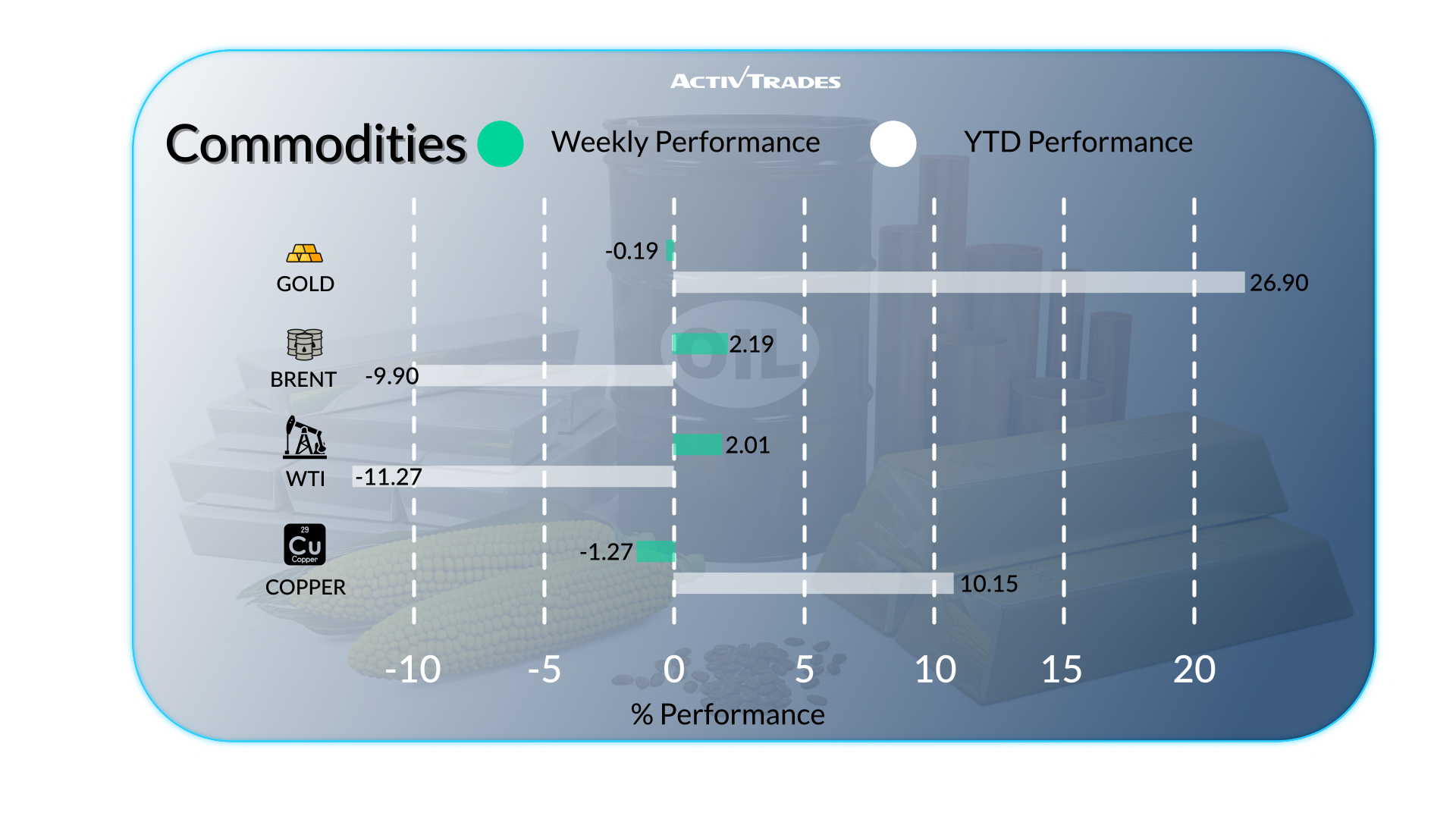

Commodities

- Oil prices are up after 2 weeks down.

- Platinum prices are up for the 3rd week in a row.

- Oats prices are down for the 7th week in a row.

- Cocoa prices are down more than 7.5%.

- Coffee prices are up more than 8%.

Indices

- The Swi20 is up for the 3rd week in a row.

- The ChinaA50 is up more than 3.10%.

- The Aus200 is up for the 3rd week in a row and hit new record highs.

- The UsaTec is down more than 2.45%.

Shares

Tops

- Dayforce: +30.56%

- P.Acurar: +16.91%

- Minerva: +11.64%

- UnitedHealth: +11.49%

Flops

- Applied Materials: -14.92%

- Palentir Technologies: -14.38%

- Strategy: -11.16%

This Week’s News to Follow

Monday 25 August

- 08:00 AM - German Ifo Business Climate (August)

- Previous: 88.6

- Forecast: 87

Tuesday 26 August

- 01:30 AM - Australian RBA Meeting Minutes

- 12:30 PM - American Durable Goods Orders MoM (July)

- Previous: -9.3%

- Forecast: -4%

Wednesday 27 August

- 06:00 AM - German GfK Consumer Confidence (September)

- Previous: -21.5

- Forecast: -23

Thursday 28 August

- 12:30 PM - American GDP Growth Rate QoQ 2nd Est (Q2)

- Previous: -0.5%

Forecast: 3%

Friday 29 August

- 05:00 AM - Japanese Consumer Confidence (August)

- Previous: 33.7

- Forecast: 34.2

- 06:45 AM - French Inflation Rate YoY Prel (August)

- Previous: 1%

- Forecast: 1.1%

- 09:00 AM - Italian Inflation Rate YoY Prel (August)

- Previous: 1.7%

- Forecast: 1.8%

- 12:00 PM - German Inflation Rate YoY Prel (August)

- Previous: 2%

- Forecast: 2.1%

- 12:30 PM - Canadian GDP Growth Rate Annualized (Q2)

- Previous: 2.2%

- Forecast: 0.2%

- 12:30 PM - Canadian GDP Growth Rate QoQ (Q2)

- Previous: 0.5%

- Forecast: 0.2%

- 12:30 PM - American Core PCE Price Index MoM (July)

- Previous: 0.3%

- Forecast: 0.3%

- 12:30 PM - American Personal Income MoM (July)

- Previous: 0.3%

- Forecast: 0.4%

- 12:30 PM - American Personal Spending MoM (July)

- Previous: 0.3%

- Forecast: 0.5%

Major Earnings Reports to Watch

Wednesday 27 August

- Salesforce

- NVIDIA

Thursday 28 August

- Best Buy

- Dell

- Dollar General

Source: Trading Economics, The Wall Street Journal, TradingView and ActivTrades’ Data as of 22 August 2025

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.