Isaac Newton's third law of motion states that for every action there is an equal but opposite reaction.

Newton was describing the physical properties of force. He noted that if one object pushes on another, then there is a reaction from that object in the other direction.

That may be a law of physics, but it sounds very much like the “cause and effect” we see playing out in the markets every day, i.e., action and reaction.

The larger the force (shock), the larger the reaction

In recent weeks, we’ve experienced a shock to the system in the shape of a war in the Middle East; sadly, that’s nothing new. However, this time it doesn't just involve regional participants but also the world superpower, the USA.

The US, in conjunction with Israel, are seeking to deny access to nuclear weapons to Iran, but also to effect regime change and to remove the religious theocracy that has ruled Iran since 1979.

However, as Prussian field marshal Helmuth von Moltke observed in 1871:

“ No operational plan survives the first encounter with the enemy intact”

And operation “Epic Fury” is no different; we are already seeing signs of mission creep.

The war on Iran isn’t going to plan, and may now drag on for much longer than expected, and not achieve its ultimate goals.

If the war is the cause, what are the effects on the markets? And they are all negative?

The war has created uncertainty and driven fuel and energy prices higher; in turn, that creates fears about the return of high inflation.

If the war is prolonged, then there are legitimate fears about global growth, particularly if the Strait of Hormuz remains closed to most traffic.

JP Morgan reminded the market this week that energy shocks lead to demand destruction, and by its estimates, some 11.0% of global oil and gas production is now off limits, thanks to the war.

The banks' analysts have also looked at the likely effect of higher energy prices on US earnings and GDP.

They conclude that each sustained +10.0% rise in the oil price will knock between 15 and 20 basis points (0.15 to 0.20%) off of US GDP.

As far as earnings are concerned, JPM calculates that if oil prices stay around $110 (Brent) for the rest of the year, then EPS (earnings per share) estimates could be downgraded by as much as -5.0%.

Against that background, it’s no surprise that US equities are hesitant: with the S&P 500 testing back to its 200-day moving average (see below).

Renowned trader Paul Tudor Jones famously said that “ Nothing good ever happened below the 200-day”

On the 200 D MA

Information technology, which had led the rally in US equities until November 25, has retraced, year to date, and the sector index now finds itself at key support levels.

Sentiment has changed, and even good news, such as blowout earnings from memory maker Micron MU, were overlooked in favour of concerns about the firm's ambitious capex plans.

That, despite a global shortage of memory chips, a key component of AI chips and servers.

The S&P 500 Information Technology sector is at a key support level.

Sentiment and market breadth look bearish, based on the S&P 500 constituents' MA percentages.

(that's the number of stocks trading above a given moving average) Those MA percentages are largely low and trending down.

The picture is pretty similar in the broader market, too. Here, we see the bullish percentage reading for stocks within the Russell 3000 index, which captures 98.0% of US market cap. Once again, the trend is lower.

Consumers to feel the pinch?

U.S. mortgage rates are rising once more and, in some cases, are breaking above long-term downtrends.

Energy markets are elevated and in a state of flux. oil and European natural gas contracts are among the biggest gainers, which inevitably has consequences.

Dutch Bank ING recently looked at the cost of filling up a car in the EU, and they found that:

“Even before oil prices reached this week’s painful highs, the jump in retail fuel prices had already pushed the cost of a standard 50‑litre tank of petrol to levels last seen in 2022 in several major eurozone economies.

Compared with the week before the joint US‑Israeli strike on Iran, the price of a tank of unleaded petrol has risen by between €4.50 in Italy and €13.00 in Germany. For diesel, the increase has been even steeper, ranging from €8.40 in Italy to €21.50 in Germany.

Relative to the 2025 annual average, German households have been hit particularly hard: they are now paying roughly €17.00 more per tank of unleaded petrol and around €28.00 more for diesel than they did on average last year. Dutch households are facing a similarly sharp increase in fuel costs.”

Source: INGThink

Energy markets period percentage changes

Source: Trading Economics

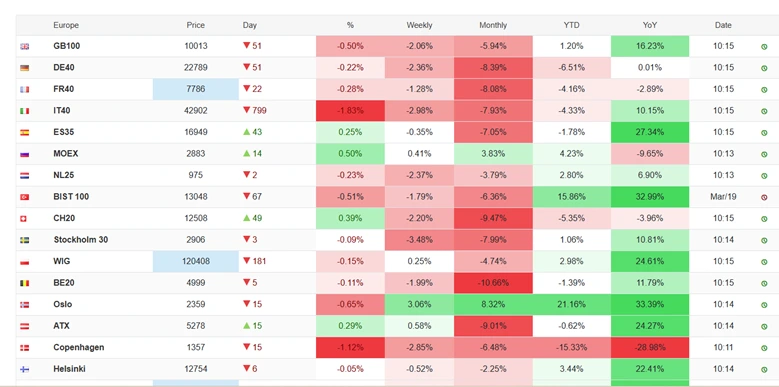

Several European equity indices have slipped into the red year to date, and much of that weakness is being driven by those higher energy costs. But note that Oslo (Norway) is up by +21.16% year to date at the time of writing.

Source: Trading Economics

Why is that?

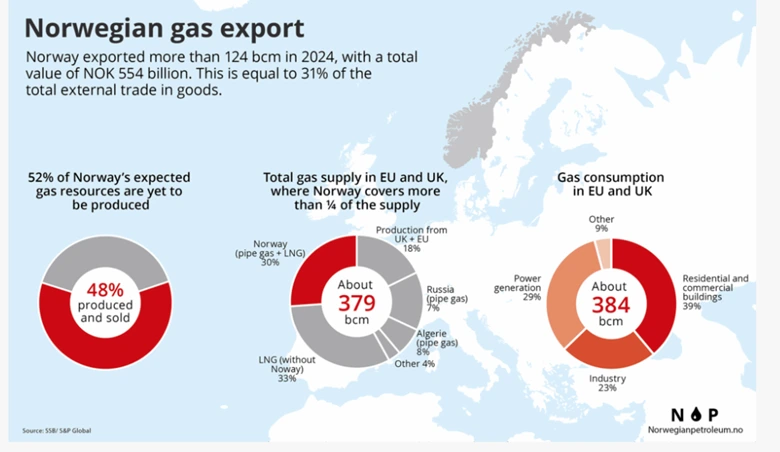

Well, Norway is largely self-sufficient when it comes to energy. Indeed, Norway is a big exporter of natural gas. In fact, Norway supplies around 30.0% of the gas consumed by the UK and Europe.

And more than half of Norway's gas reserves are still in the ground, whilst Middle East production is being hampered by the war.

Qatari authorities have suggested that it could take many months, or even years, before their gas production and processing are back to pre-war levels.

Source: NorskPetroleum

Norway is in a strong position.

The Norwegian Krona is up by more than +9.0% against the US dollar in the last 12 months and by more than +11.0% versus the Euro.

USD/NOK (scale inverted)

Source: Trading Economics

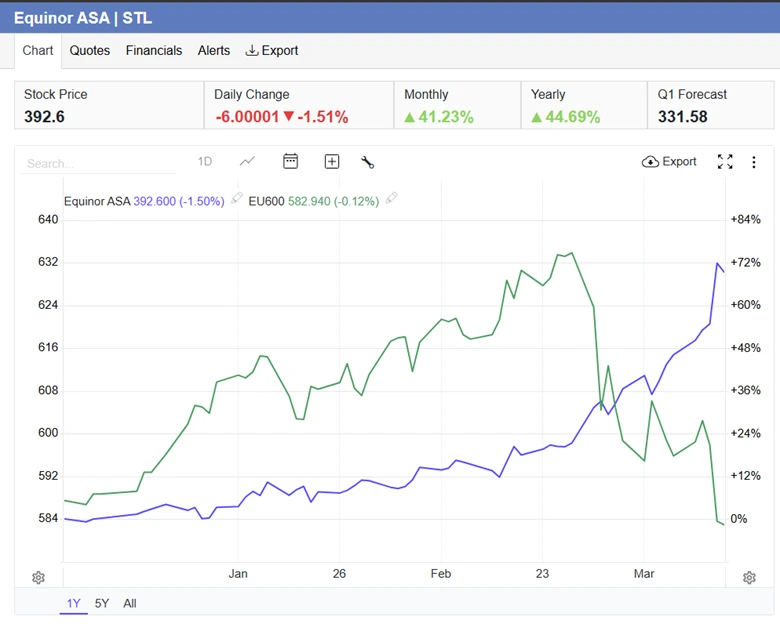

Here is the Norwegian oil company Equinor (blue) compared to the Stoxx 600 index (green) that tracks major companies across Europe. The chart shows the percentage change in both instruments.

Source: Trading Economics

Asia is not immune

It's not just Europe that's been hit hard by the war and energy price rises. Asia has been affected too.

South Korea is estimated to be the 3rd largest importer of LNG (Liquefied Natural Gas) in the world.

Around 15.0% of that gas comes from Qatar. Or at least it did.

Korea may be able to boost the volume of gas it imports from Australia and Malaysia to cover that shortfall.

But of course, it will compete with other economies, both in Asia and elsewhere, that are also looking to replace Middle Eastern gas that's no longer available to them.

Korean officials insist that they won't suffer a supply disruption following Iran's attacks on Qatari LNG facilities, but it's hard to see how that can be true with things as they are.

EWY US is the iShares MSCI South Korea ETF.

As you can see below, it has undergone a sharp correction in recent weeks.

Once again, this is an index that’s led by technology and memory chip makers; Samsung and SK Hynix make up more than half of the index.

However, that’s turned out to be both a blessing and a curse; on the one hand, a global shortage of memory chips provided the Korean manufacturers with pricing power, which they have been happy to exercise.

But on the other hand, a short fall in LNG imports could destabilise local power markets, and nobody wants to have to choose between heating or cooling homes and running production lines later this year.

Source: Barchart

There are already winners and losers in this war regardless of the outcome. Energy security is becoming increasingly important. Those countries which have large reserves of oil and gas, but are not located in the Middle East, are the likely winners. However, those who are reliant on energy imports, whether from the Persian Gulf or further afield, are the ones who are likely to be the losers.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.