Weekly Outlook

What Happened This Week?

Global

● The war involving Iran is weighing on global markets as investors fear a broader conflict that could push oil prices higher, slow growth, and complicate the global inflation outlook.

● Higher energy prices and rising government bond yields following the conflict are increasing borrowing costs worldwide.

● The International Monetary Fund said the economic impact of the conflict remains uncertain and will provide a full assessment next month. It previously projected global growth of 3.3%.

United States

● The U.S. manufacturing sector expanded for a second straight month in February, with the ISM index at 52.4. Backlogs reached their highest level since May 2022, while the prices index rose to its highest reading since June 2022.

● Services activity strengthened, with the ISM services index rising to 56.1 in February from 53.8 in January. New orders and business activity reached their highest levels of 2024.

● The Federal Reserve’s Beige Book reported steady economic activity, persistent inflation pressures, and a generally stable labor market across all 12 districts.

● ADP reported 63,000 private-sector jobs added in February, following a revised 11,000 increase in January.

● Initial jobless claims remained stable at 213,000, while continuing claims rose to 1.87 million.

● New York Fed President John Williams said recent rate cuts have left policy well calibrated but noted that further easing may be needed if inflation cools.

● Minneapolis Fed President Neel Kashkari said one or two rate cuts could occur if inflation slows, but the Iran conflict could justify delaying easing.

● Kashkari said the current policy range of 3.5%–3.75% is close to neutral and added that tariffs have not yet shown clear inflationary effects.

● Fed Chair Jerome Powell accused the Justice Department of threatening him with an indictment over pressure to cut rates, an episode that has intensified concerns about central-bank independence.

China

● China set its 2026 GDP growth target at 4.5%–5%, the lowest level in decades, reflecting weaker domestic demand, subdued investment, and a struggling property sector.

● Premier Li Qiang identified boosting domestic consumption as the government’s top economic priority for 2026 and announced new financing tools to support growth.

● The National People’s Congress is expected to approve a five-year economic strategy aimed at turning China into a technological superpower.

● China’s official manufacturing PMI fell to 49.0 in February from 49.3 in January, signaling continued contraction.

● The non-manufacturing PMI edged up slightly to 49.5 as service activity benefited from Lunar New Year spending.

Asia

● Manufacturing activity across Asia improved in February, supported by strong global demand and the rapid expansion of artificial-intelligence related industries.

● Taiwan’s manufacturing output grew at its fastest pace in more than 4.5 years.

● Japan’s factory activity reached a 45-month high.

● Strong export performance and leadership in the AI supply chain continue to support the region’s outlook for 2026.

Japan

● Bank of Japan Governor Kazuo Ueda reaffirmed the central bank’s commitment to further interest-rate hikes despite rising geopolitical risks.

● Policymakers are closely monitoring the yen, as currency weakness could push import-driven inflation higher.

● The Middle East conflict is seen as a potential source of economic and inflation volatility for Japan.

Eurozone

● Inflation unexpectedly accelerated to 1.9% year-over-year in February, up from 1.7% in January, with higher energy prices posing additional upside risks.

● Eurozone retail sales fell 0.1% in January despite improving consumer confidence and record-low unemployment.

● ECB Vice President Luis de Guindos said the central bank could adjust its policy stance if inflation trends change significantly.

● Austria’s central bank governor said the ECB must be ready to move interest rates quickly in either direction if uncertainty intensifies.

United Kingdom

● U.K. Treasury Chief Rachel Reeves said the government remains on track to reduce borrowing, with the fiscal deficit projected at 4.3% of GDP, the lowest since the pandemic.

● Rising energy prices linked to the Iran conflict could weaken growth while pushing inflation and borrowing costs higher.

Canada

● Canada and India signed agreements to strengthen cooperation in energy, critical minerals, and trade in an effort to diversify Canada’s economic partnerships beyond the U.S.

● A C$2.6 billion agreement will see Cameco supply uranium to India from 2027 to 2035.

● Both countries aim to double bilateral trade to C$70 billion by 2030 under a new Comprehensive Economic Partnership Agreement.

● Canada’s manufacturing PMI rose to 51 in February, indicating a second month of expansion.

● Domestic demand supported new orders for the first time in 13 months, although U.S. tariffs continue to weigh on export sales.

● Canadian labor productivity fell 0.1% in Q4 2025, while business GDP declined 0.2% during the quarter.

Australia

● Australia’s economy grew 0.8% in the fourth quarter and 2.6% year-over-year, reinforcing expectations of further monetary tightening.

● The Reserve Bank of Australia raised rates in February after inflation remained above its 2%–3% target.

● Governor Michele Bullock said every policy meeting remains “live” as markets increase bets on another rate hike.

Switzerland

● Swiss inflation remained at 0.1% year-over-year in February, unchanged from January, raising concerns about persistent disinflation.

● The Swiss National Bank signaled a greater willingness to intervene in foreign-exchange markets as the franc strengthened more than 14% against the dollar over the past year.

Malaysia

● Bank Negara Malaysia kept its benchmark interest rate unchanged at 2.75% for the fourth consecutive meeting, citing stable domestic conditions and global uncertainty.

Ireland

● Ireland’s economy contracted 3.8% in the fourth quarter of 2025, a larger decline than previously estimated, though full-year GDP still increased 12.3%.

This Week’s Market Movers

Forex

● Rising tensions in Iran have pushed the dollar toward its strongest weekly performance in twelve months as demand for "safe-haven" assets surges.

● The South Korean won hit a 17-year low, sliding below 1,500 per dollar for the first time since the global market crash of 2009.

● The EUR/USD is down more than 1.40%.

● The NZD/CAD is down more than 1.20%.

● The USD/HUF is up more than 4.60%.

● The USD/ZAR is up more than 3.95%.

● The USD/RUB is up more than 3%.

● The CAD/EUR is up more than 1.70%.

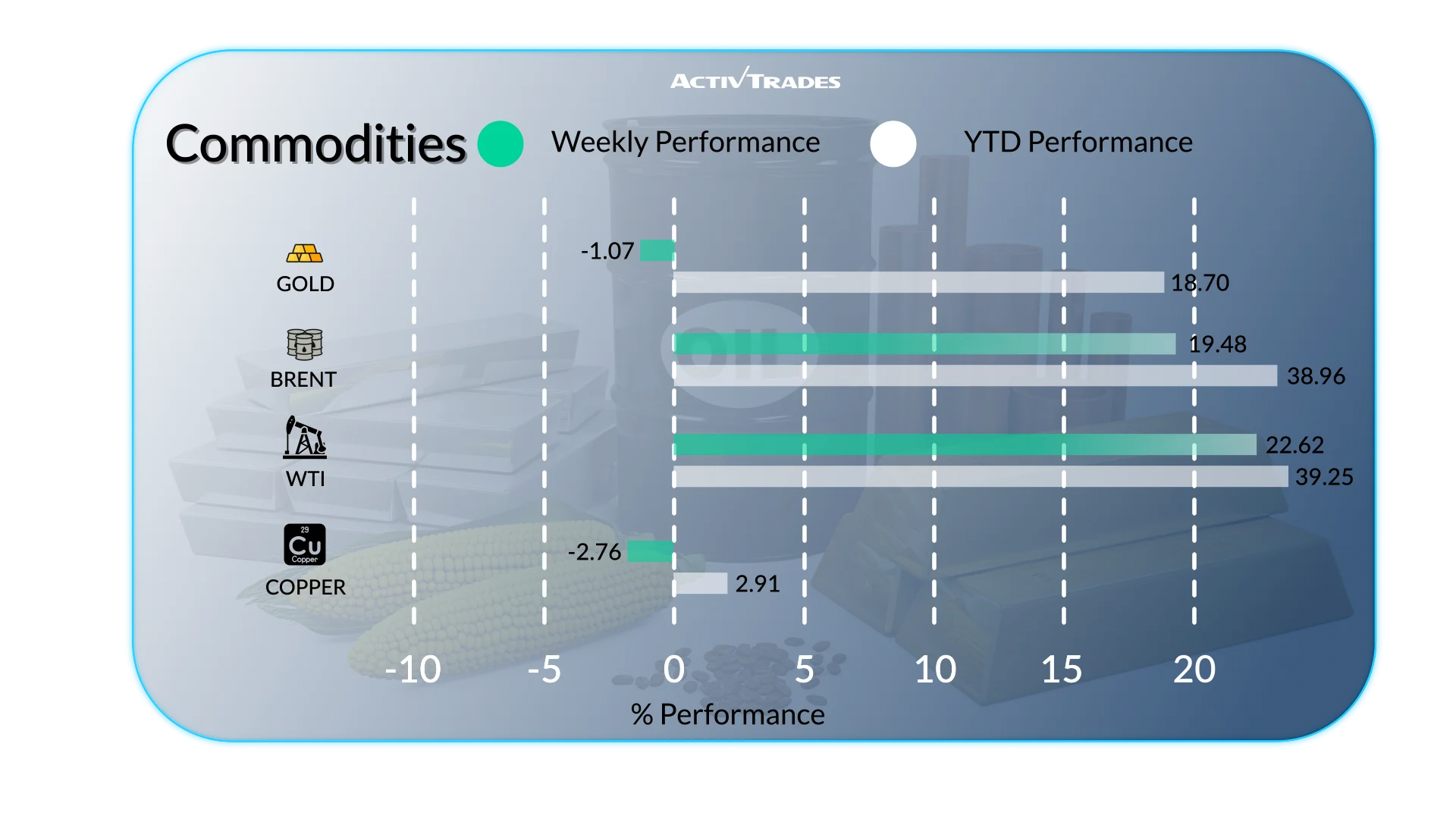

Commodities

● Heating oil prices are up more than 30%.

● Brent prices are up more than 17% and Crude prices are up around 20%.

● Silver prices and Platinum prices are down more than 9%.

● Aluminium prices are up more than 5%.

● Cocoa prices are up more than 7%.

● Oats prices are up more than 6%.

● Coffee prices are up more than 5%.

Indices

● The VIX index is up more than 30%.

● The KOSPI index is down more than 9%.

● The Euro50 index is down more than 6.30%.

● The CAC 40 index is down more than 6.10%.

● The Bovespa index is down more than 5.60%.

● The DAX 40 index and the Japan225 index are down more than 5.10%.

Shares

Tops

● Trade Desk: +41.18%

● Braskem: +32.98%

● Block: +29.08%

● Expedia Group: +22.74%

● Applovin: +20.89%

● Intuit: +20.31%

● Netflix: +19.19%

● CrowdStrike: +16.04%

● Autodesk: +15.63%

● Palentir Technologies: +14.06%

● Deutsche Boerse: +10.16%

Flops

● Beiersdorf: -21.61%

● Hikma Pharmaceuticals: -19.49%

● Melrose Industries: -18.12%

● Qnity Electronics: -17.15%

● United Airlines: -16.94%

● Carnival: -15.65%

● Ciena: -15.59%

● Minerva: -14.39%

● Company de Saint Gobain: -13.37%

● Commerzbank: -12.71%

Important Events to Follow

Monday 09 March

● 01:30 AM - Chinese - Inflation Rate YoY (February)

○ Previous: 0.2%

○ Forecast: 0.4%

● 11:30 PM - Australian - Westpac Consumer Confidence Change (March)

○ Previous: -2.6%

○ Forecast: -1.1%

Tuesday 10 March

● 12:30 AM - Australian - NAB Business Confidence (February)

○ Previous: 3

○ Forecast: 3

● 03:00 AM - Chinese - Balance of Trade (January-February)

○ Previous: $114.1B

○ Forecast: $1.6B

● 03:00 AM - Chinese - Exports YoY (January-February)

○ Previous: 6.6%

● 03:00 AM - Chinese - Imports YoY (January-February)

○ Previous: 5.7%

● 07:00 AM - German - Balance of Trade (January)

○ Previous: €17.1B

○ Forecast: €15.4B

● 02:00 PM - American - Existing Home Sales (February)

○ Previous: 3.91M

○ Forecast: 3.90M

Wednesday 11 March

● 12:30 PM - American - Core Inflation Rate YoY (February)

○ Previous: 2.5%

○ Forecast: 2.5%

● 12:30 PM - American - Inflation Rate YoY (February)

○ Previous: 2.4%

○ Forecast: 2.4%

Thursday 12 March

● 12:30 PM - American - Building Permits Prel (January)

○ Previous: 1.455M

○ Forecast: 1.433M

● 12:30 PM - American - Housing Starts (January)

○ Previous: 1.404M

○ Forecast: 1.37M

Friday 13 March

● 07:00 AM - UK - GDP MoM (January)

○ Previous: 0.1%

○ Forecast: 0.1%

● 12:30 PM - Canadian - Unemployment Rate (February)

○ Previous: 6.5%

○ Forecast: 6.7%

● 12:30 PM - American - Core PCE Price Index MoM (January)

○ Previous: 0.4%

○ Forecast: 0.3%

● 12:30 PM - American - Durable Goods Orders MoM (January)

○ Previous: -1.4%

○ Forecast: 0.3%

● 12:30 PM - American - GDP Growth Rate QoQ 2nd Est (Q4)

○ Previous: 4.4%

○ Forecast: 1.4%

● 12:30 PM - American - Personal Income MoM (January)

○ Previous: 0.3%

○ Forecast: 0.2%

● 12:30 PM - American - Personal Spending MoM (January)

○ Previous: 0.4%

○ Forecast: 0.3%

● 02:00 PM - American - JOLTs Job Openings (January)

○ Previous: 6.542M

○ Forecast: 6.5M

● 02:00 PM - American - Michigan Consumer Sentiment Prel (March)

○ Previous: 56.6

○ Forecast: 55

Major Earnings Reports to Watch

Monday 09 March

● Hewlett Packard

Tuesday 10 March

● Oracle

● Volkswagen

● Phoenix

● Hugo Boss

● BioNTech

Wednesday 11 March

● Rheinmetall

Thursday 12 March

● Zalando

● ADOBE

● Hannover Rueck

● Dollar General

● BMW

● RWE

● Swiss Life

● Vivendi

● Daimler

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of March 6, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.