Weekly Outlook

What Happened This Week?

United States

- U.S. services sector continued to expand in April, with the ISM services PMI at 53.6 versus 54.0 in March.

- The ISM prices index remained at 70.7, its highest level since October 2022, highlighting persistent inflation pressures.

- Employment in the services sector contracted for a second straight month, despite growth across 14 industries.

- U.S. jobless claims rose to 200,000 in the week ending May 2, while continuing claims eased slightly to 1.77 million.

- ADP reported 109,000 private-sector jobs added in April, the strongest reading in 15 months and above expectations.

- Hiring improved in March, but job openings continued to trend lower, keeping the labor market in a “low-hire, low-fire” environment.

- The Labor Department said the job openings rate slipped to 4.1% in March, while the hiring rate improved to 3.5%.

- Fed Chair Jerome Powell said stronger labor-market data allows the Fed to focus more on inflation risks.

- U.S. services inflation and energy costs remain key concerns for the Federal Reserve as gasoline prices continue rising.

- The national average gasoline price reached $4.54 per gallon, up 52% since the initial Iran conflict escalation.

- Economists warned higher fuel prices are acting as a tax on consumers and could weigh on spending ahead.

- Sales of new single-family homes rose to 682,000 in March, beating expectations.

- The median new-home price fell 5.3% month over month to $387,400.

- New-home inventory declined slightly to 481,000 units in March.

- Spirit Airlines’ collapse is expected to reduce competition and potentially push airfares higher as airlines pass rising fuel costs to consumers.

Eurozone

- Eurozone retail sales unexpectedly fell 0.1% in March as higher fuel costs weighed on spending.

- Consumer confidence dropped to its lowest level since December 2022 in April, signaling weaker demand ahead.

- Eurozone inflation accelerated to 3.0% in April from 1.9% in February due to rising energy prices linked to the Iran conflict.

- ECB official Francois Villeroy de Galhau said markets may be misreading the ECB’s intentions regarding a June rate hike.

- Villeroy stressed that ECB policy decisions remain data-dependent and warned attacks on central-bank independence could damage credibility.

- ECB data showed eurozone wage growth is expected to slow to 2.6% in 2026 from 3.0% in 2025.

- ECB officials remain concerned that persistent energy inflation could fuel higher wage demands and strengthen the case for rate hikes.

Germany

- German manufacturing orders rose 5.0% in March, beating expectations and marking a second consecutive monthly increase.

- Economists said businesses are building inventories amid fears of supply disruptions and higher prices linked to the Middle East conflict.

- Despite stronger orders data, rising energy prices continue to threaten Germany’s industrial recovery.

Switzerland

- Swiss inflation rose to 0.6% in April, the highest level since December 2024, driven by imported energy costs.

- Petroleum prices surged 17% year over year.

- Markets are now pricing in one Swiss National Bank rate hike this year, reducing expectations for negative rates.

United Kingdom

- No major U.K. data release this week, but investors continue monitoring energy-driven inflation pressures and growth risks tied to the Middle East conflict.

Canada

- No major Canadian macroeconomic release dominated this week, though markets remain focused on inflation expectations and energy-price pressures.

Mexico

- The Bank of Mexico cut its benchmark interest rate to 6.5%, signaling this was likely the final cut in the current easing cycle.

- The board voted 3-2 in favor of the quarter-point cut.

- Policymakers cited softer inflation in April and a larger-than-expected first-quarter economic contraction.

Norway

- Norges Bank raised its key policy rate to 4.25% from 4.00% to contain elevated inflation risks.

- Norway’s core inflation remained at 3.0%, above the central bank’s 2% target for more than four years.

Sweden

- Sweden’s Riksbank kept its key policy rate unchanged at 1.75%.

- Policymakers maintained a cautious stance despite rising inflation risks tied to the Middle East conflict.

Switzerland

- Swiss inflation climbed to 0.6% in April, reinforcing expectations the SNB may tighten policy later this year.

Australia

- The Reserve Bank of Australia raised its cash rate by 25 basis points to 4.35%.

- The RBA warned inflation risks remain skewed to the upside and are likely to stay above target.

- Household spending rose 1.6% in March, marking the strongest increase in 30 months.

China / Hong Kong

- Hong Kong’s economy expanded 5.9% year over year in Q1 2026, the fastest pace in nearly five years.

- Officials credited exports and AI-related demand as key growth drivers.

- Authorities warned ongoing Middle East tensions remain a downside risk for growth.

Malaysia

- Bank Negara Malaysia kept its policy rate unchanged at 2.75%.

- Policymakers cited contained inflation and resilient domestic conditions despite external uncertainties.

- Fuel subsidies continue helping limit inflation pressures.

Indonesia

- Bank Indonesia tightened dollar-purchase rules, limiting monthly domestic FX purchases to $50,000 per person.

- The central bank pledged more FX intervention to support the rupiah, which officials described as undervalued.

- Analysts said the measures may provide temporary support, but broader external risks remain.

Global

- Rising energy prices linked to the Iran conflict continue driving inflation pressures globally.

- Central banks across developed and emerging markets remain cautious as higher oil prices complicate policy decisions.

- Markets remain focused on inflation trends, energy prices, and the risk of further monetary tightening globally.

This Week’s Market Movers

Forex

- The NZD/CAD and the ZAR/JPY are up more than 1.30%.

- The USD/RON is up more than 1.40%.

- The GBP/UHF is down more than 2.60%.

- The EUR/UHF is down more than 2.40%.

- The CAD/NZD is down more than 1.20%.

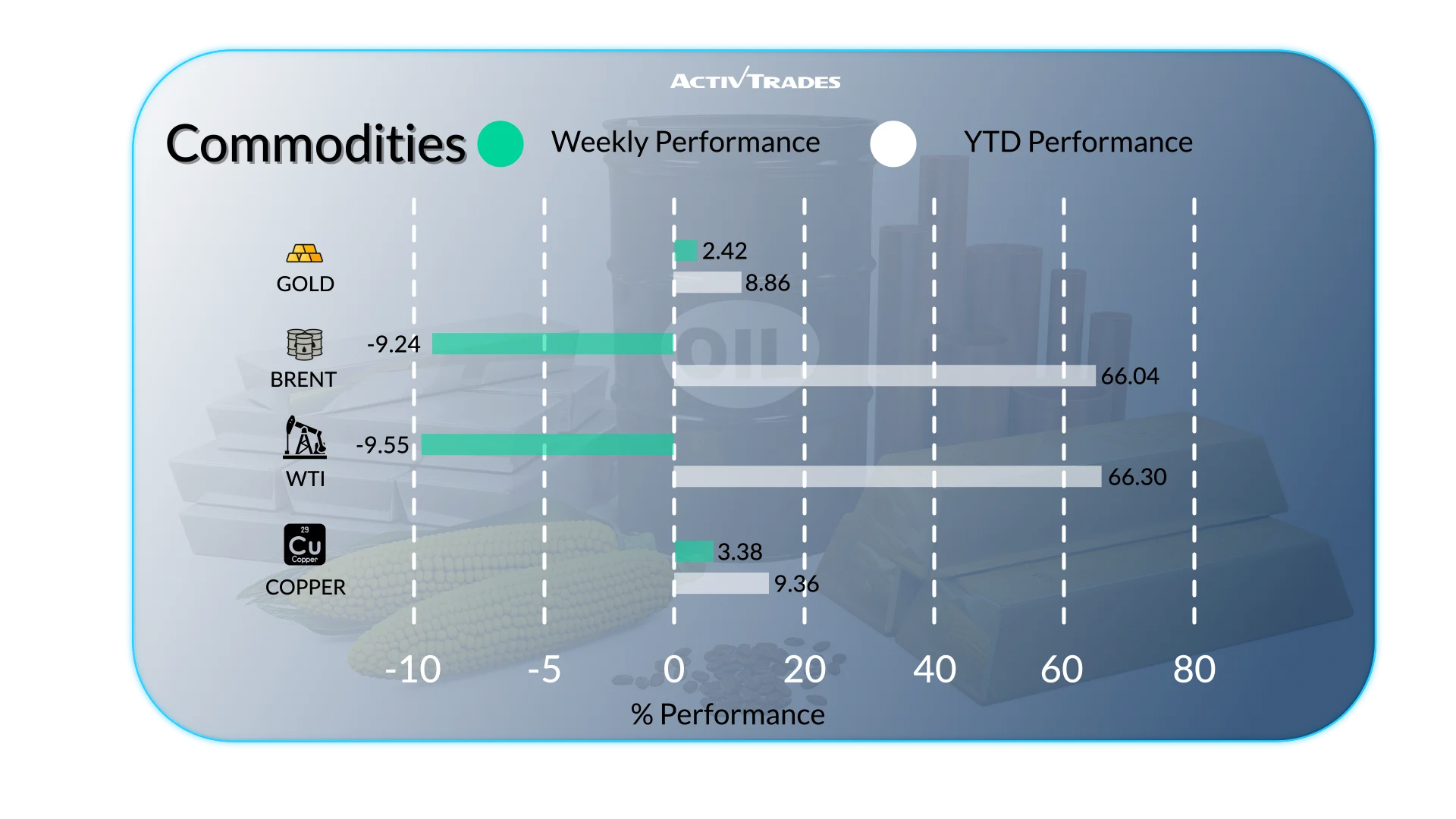

Commodities

- US Cocoa prices are up more than 21%.

- Copper and Silver prices are up more than 5%.

- Orange Juice prices are down more than 7.80%.

- Brent prices are down more than 7%.

- WTI prices are down more than 6.50%.

- Coffee prices are down more than 4.80%.

Indices

- The KOSPI index is up more than 11%.

- The Japan 225 index is up more than 5.50%.

- The Dax index is up more than 4%.

- The VIX index is down more than 8.50%.

Shares

Tops

- Datadog: +41.85%

- DaVita: +29.63%

- Fortinet: +26.84%

- Super Micro Computer: +24.93%

- Healthpeak Properties: +22.80%

- Micron Technology: +22.07%

- Sandisk: +20.45%

- Smarfit Escola de Gastica e Danca: +20.05%

- Fresnillo: +17.07%

- Endeavour Mining: +16.41%

- Rolls-Royce: +14.60%

- MTU Aero Engines: +13.48%

- Safran: +11.62%

Flops

- Ismed: -23.41%

- Zoetis: -23.44%

- CDW: -18.49%

- Arista Networks: -17.59%

- Cencora: -16.98%

- Huntington Ingalis Industries: -13.87%

- Pool: -10.93%

Important Events to Follow

Monday 11 May

- 01:30 AM - Chinese - Inflation Rate YoY (April)

- Previous: 1%

- Forecast: 0.8%

- 02:00 PM - American - Existing Home Sales (April)

- Previous: 3.98M

- Forecast: 4.05M

Tuesday 12 May

- 12:30 AM - Australian - Westpac Consumer Confidence Change (May)

- Previous: -12.5%

- Forecast: 1.1%

- 01:30 AM - Australian - NAB Business Confidence (April)

- Previous: -29

- Forecast: -32

- 09:00 AM - German - ZEW Economic Sentiment Index (May)

- Previous: -17.2

- Forecast: -26

- 12:30 PM - American - Core Inflation Rate YoY (April)

- Previous: 2.6%

- Forecast: 2.6%

- 12:30 PM - American - Inflation Rate YoY (April)

- Previous: 3.3%

- Forecast: 3.6%

Wednesday 13 May

- 12:30 PM - American - PPI MoM (April)

- Previous: 0.5%

- Forecast: 0.4%

Thursday 14 May

- 06:00 AM - UK - GDP Growth Rate YoY Prel (Q1)

- Previous: 1%

- Forecast: 1.4%

- 06:00 AM - UK - GDP MoM (March)

- Previous: 0.5%

- Forecast: 0.2%

- 12:30 PM - American - Retail Sales MoM (April)

- Previous: 1.7%

- Forecast: 0.1%

Major Earnings Reports to Watch

Monday 11 May

- Hannover Rueck

- Gold Resource

Tuesday 12 May

- JD.com

- KBC Group

- ThyssenKrupp

- ACS Actividades de Construccion y Servicios

- Muenchener Rueckversicherungs

- Bayer

- Phoenix

Wednesday 13 May

- Alibaba

- CISCO

- Sumitomo Mitsui Financial

- ABN AMRO

- Siemens

- E.ON

- Deutsche Telekom

- Allianz

- RWE

- Alstom

Thursday 14 May

- Honda Motor

- Telefonica

- 3i Group

Friday 15 May

- Mitsubishi UFJ Financial

- Mizuho Financial

- Semapa-Sociedade De Investim

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of May 08, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.