As the trading year draws to a close and the holiday period begins in earnest we will get the chance to think about what 2023 will bring and what will be important to traders in the new year.

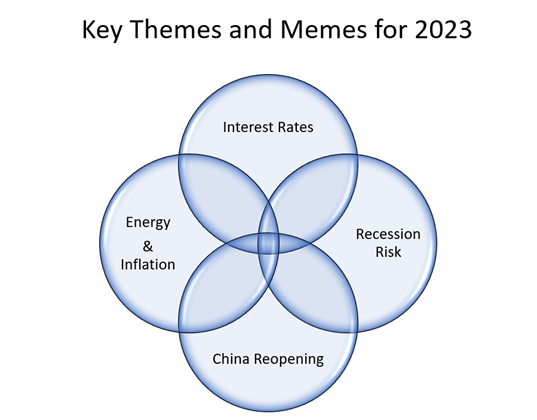

To my mind, there are four key macroeconomic themes that are likely to dominate next year's trading. Each of these themes will not only be important in its own right but, they also interlink with the other three, as we can see in the diagram below.

The level and path of US interest rates has been the dominant story during 2022 and we are ending the year with a mismatch between central bankers and the market. The Federal Reserve raised rates, in December, as anticipated, by 0.50%.

However, Fed Governor Jerome Powell implied that the central bank may need to raise US rates further than the market is forecasting and that, the idea that US rates might start to fall in the last quarter of 2023 is misplaced.

The rally in equity markets came to halt as a result of those comments.

Bond markets disagree

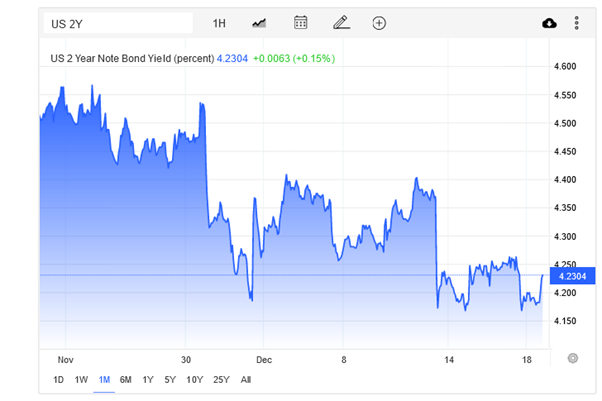

However, two-year US Treasury bonds yields continued to trend lower and that suggests that bond traders don't buy into Mr Powell's higher for longer comments.

That may be because the bond markets believe the action, that Fed has already taken, has been enough to dampen demand, and that should allow inflation to continue to cool.

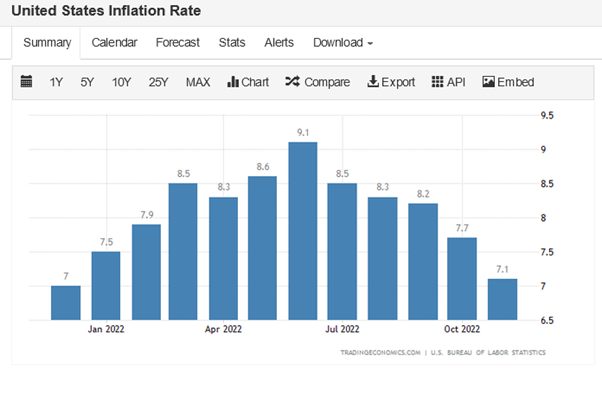

SourceTrading Economics

As demonstrated in the November inflation data, which came in below forecasts, in both the headline and core figures.

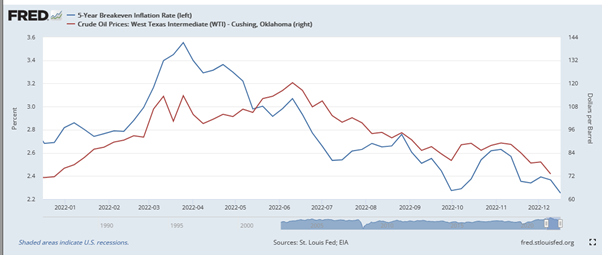

Source Fred data

Inflation expectations in the US are closely linked to the price of energy and in particular, the price of oil (WTI Crude). In the chart above we see the bond markets' 5-year-inflation expectations or, breakevens, in blue, overlaid by the price of crude oil in red.

As we can see, both have been trending lower during the second half of the year.

If they continue to do so in 2023, then that could allow the Fed to ease up on the pace and size of interest rate rises.

More than enough

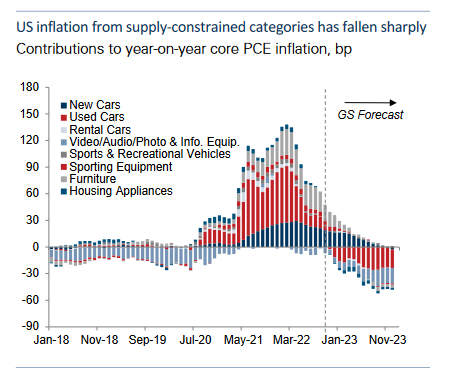

In fact, some in the market believe that US interest rates are already too high. And that any further moves in that direction have the potential to push the US economy into a recession.

They point to reductions in geopolitical tensions and supply chain constraints, which helped to drive prices higher, but which, are now fading, see the chart below.

Source Goldman Sachs research

These doves say that raising the cost of money further runs the risk of creating needless demand destruction in the US economy.

Earnings insights

We will get some insights into how US businesses view 2023, as companies report Q4 22 earnings, and offer guidance about the coming quarter.

Earnings season kicks off in mid-January.

Wall Street analysts' outlook for earnings growth, in the S&P 500, for Q4 2022, is for a -2.80% decline, which would be the first negative quarter since Q3 2020.

Earnings and economic activity are closely correlated, and so the trend and tone of Q4 earnings season and any guidance about Q1 that is provided could tell us a lot about what 2023 will hold for the US economy.

Source: Schroders

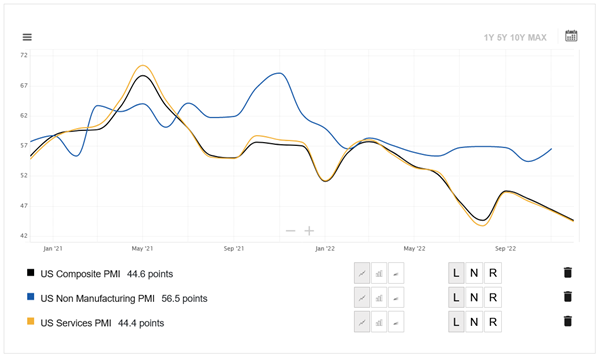

A recession in 2023 isn’t a certainty though. Survey-based data from the ISM, and S&P Global, are predicting conflicting outcomes.

The ISM US Non-manufacturing PMI showed a marked uptick in November, whilst both the S&P Composite and Services PMIs continued to fall.

Source Trading Economics

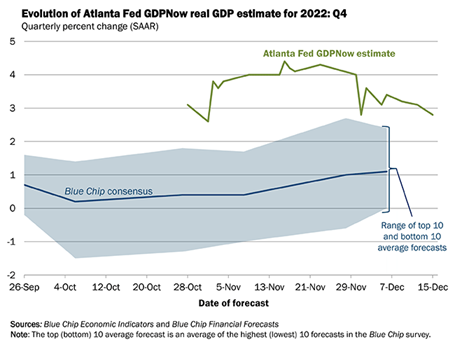

Predictions about US GDP are also at odds with each other. For example, the chart below shows the Atlanta Fed’s GDPNow estimate for Q4 GDP (in green) compared to the average forecast among economists.

And though the GDPNow forecast has been falling it still remains well above the wider consensus, shown in the blue-shaded area, and the top 10 forecasts shown by the dark blue line within it.

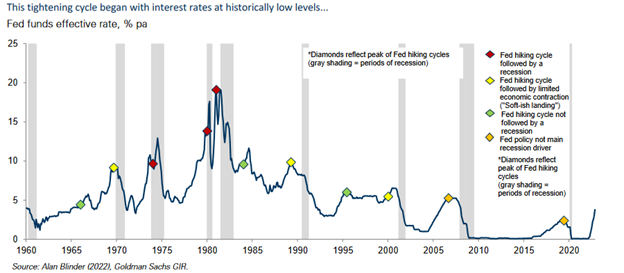

However, history suggests that some kind of economic contraction is almost inevitable, following a rate-rise cycle.

All roads lead to China

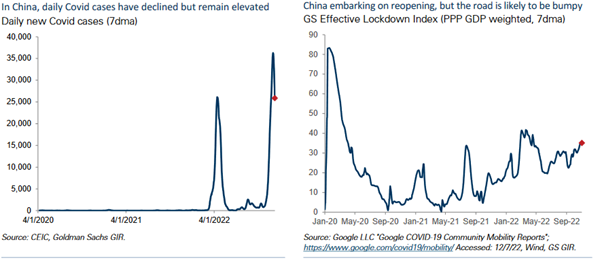

Much may depend on what happens in China and whether the authorities can re-open the economy fully, without succumbing to further waves of Covid.

Source Goldman Sachs research

New cases remain high and though lockdowns are not as restrictive as they once were. They are still hampering economic activity in China and its trade with the rest of the world.

Here is where it gets interesting!

Because a reopening of the Chinese economy would likely be inflationary, simply because it would add demand to the global economy.

That demand could help to repair a sharp decline in both Chinese exports and imports.

For example, Chinese exports to the US fell by -13.20% YoY in November. A rebound in that metric would help the economy of both parties.

However, this a double-edged sword, because heightened demand will push up the price of key commodities such as oil, and that, will feedback into expectations about US inflation, and the pace and direction of future interest rate rises.

So we could be in for an interesting year ahead.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.