Weekly Outlook

What Happened This Week?

United States

- The U.S. China Summit could reveal some agreements.

- Fed Governor Michael Barr warned that aggressively shrinking the Fed’s balance sheet could hurt financial stability and weaken bank resilience.

- Barr’s comments came after Kevin Warsh’s confirmation as Federal Reserve chair, as Warsh supports reducing the Fed’s balance sheet.

- Jerome Powell officially ended his term as Fed chair on May 15 but will remain on the Fed board despite political pressure from President Trump.

- Powell was credited with guiding the Fed through the post-pandemic inflation shock without triggering a recession, despite criticism over initially calling inflation “transitory.”

- Kevin Warsh was confirmed as the 17th Fed chair with a narrow 54-45 Senate vote.

- Warsh takes office as inflation remains elevated and questions over Fed independence intensify.

- Boston Fed President Susan Collins said rates may need to stay higher for longer, with possible hikes if inflation remains persistent.

- Three Fed officials dissented at the April meeting, favoring language that acknowledged possible future rate hikes.

- U.S. wholesale inflation rose 1.4% in April, pushing the annual producer-price inflation rate to 6.0%, the highest since late 2022.

- Wholesale energy prices surged 7.8% in April as the Iran conflict continued lifting oil prices.

- The producer-price data reinforced expectations that the Fed’s preferred inflation gauge will remain above target.

- U.S. retail sales growth slowed to 0.5% in April from 1.6% in March as gasoline price increases moderated slightly.

- Consumer inflation accelerated to 3.8% year over year in April, the highest level in three years.

- Existing-home sales rose 0.2% in April to an annualized pace of 4.02 million but missed forecasts.

- Mortgage rates climbed back to 6.37% due to rising energy prices and inflation concerns linked to the Iran conflict.

- The labor market remained resilient, with the U.S. economy adding 115,000 jobs in April.

- Initial jobless claims rose by 12,000 to 211,000 in the week ending May 9.

- Continuing claims increased to 1.78 million, while broader labor indicators continued signaling a relatively stable employment environment.

- The Conference Board’s Employment Trends Index rose to 105.77 in April, supported by historically low layoffs and stronger temporary hiring activity.

United Kingdom

- The U.K. economy expanded 0.6% in the first quarter, outperforming the U.S. and most European economies.

- Economists warned the U.K. faces growing risks from the Middle East conflict, rising energy costs, and domestic political uncertainty.

- Recent election losses increased political uncertainty and pushed government borrowing costs higher.

Eurozone

- ECB Chief Economist Philip Lane warned the global rise in energy prices could slow eurozone growth and push inflation higher.

- Lane said globally synchronized energy inflation creates additional upward pressure on European production costs and consumer prices.

- ECB officials warned persistent energy inflation could fuel stronger wage demands and trigger second-round inflation effects.

- The ECB said immigration remains critical for sustaining eurozone economic growth as the population ages.

- Eurozone industrial production rose 0.2% in March, matching February’s increase despite higher energy costs.

- The Middle East conflict forced the EU to spend an additional 27 billion euros on energy imports in March.

- The ECB lowered its 2026 eurozone growth forecast to 0.9% from 1.2% due to worsening industrial conditions.

Canada

- Bank of Canada officials said policy may need to shift quickly depending on Middle East developments and U.S. trade tensions.

- The Bank of Canada kept rates unchanged at 2.25% and expects limited policy changes if the economy evolves as forecast.

- Governor Tiff Macklem said rate cuts remain possible if new U.S. trade restrictions weaken Canada’s economy.

- Market participants now expect the Bank of Canada’s first rate hike in March 2027, earlier than previously forecast.

- A central bank survey showed inflation expectations rising to 2.6% for 2026.

Australia

- Australia’s Labor government introduced major property tax reforms, including changes to negative gearing and capital-gains tax rules.

- The government’s 2026-2027 budget also includes more than A$10 billion in fuel-security spending.

- Economists remain divided on whether the tax reforms will meaningfully improve productivity or housing affordability.

- The government plans to reduce spending on the National Disability Insurance Scheme by A$37.8 billion over four years.

- Canberra forecasts economic growth slowing to 1.75% and unemployment rising to 4.5% by midyear.

China

- The People’s Bank of China warned imported inflation risks are increasing due to rising global oil and commodity prices.

- The central bank reiterated its commitment to maintaining a “moderately loose” monetary-policy stance.

- China’s factory-gate inflation rose 2.8% year over year in April, ending a 41-month producer-price deflation cycle.

- Consumer inflation accelerated to 1.2% in April from 1.0% in March.

- Officials said stronger oil prices and increased travel demand contributed to higher inflation.

- The PBOC acknowledged China’s first-quarter growth remained uneven and too dependent on exports rather than domestic demand.

Global

- Global foreign direct investment increased 15% to $1.7 trillion, the highest level since 2021, according to the OECD.

- Rising energy prices linked to the Middle East conflict continue driving inflation risks and slowing global growth expectations.

- Central banks globally remain increasingly cautious as inflation pressures broaden beyond energy markets.

This Week’s Market Movers

Forex

- The USD/SEK is up more than 1.8%.

- The CHF/SEK is up more than 1.2%.

- The USD/JPY and AUD/GBP are up more than 1%.

- The EUR/RUB is down more than 2.3%.

- The GBP/RON is down more than 1.8%.

- The GBP/USD is down more than 1.4%.

- The NZD/USD is down more than 1%.

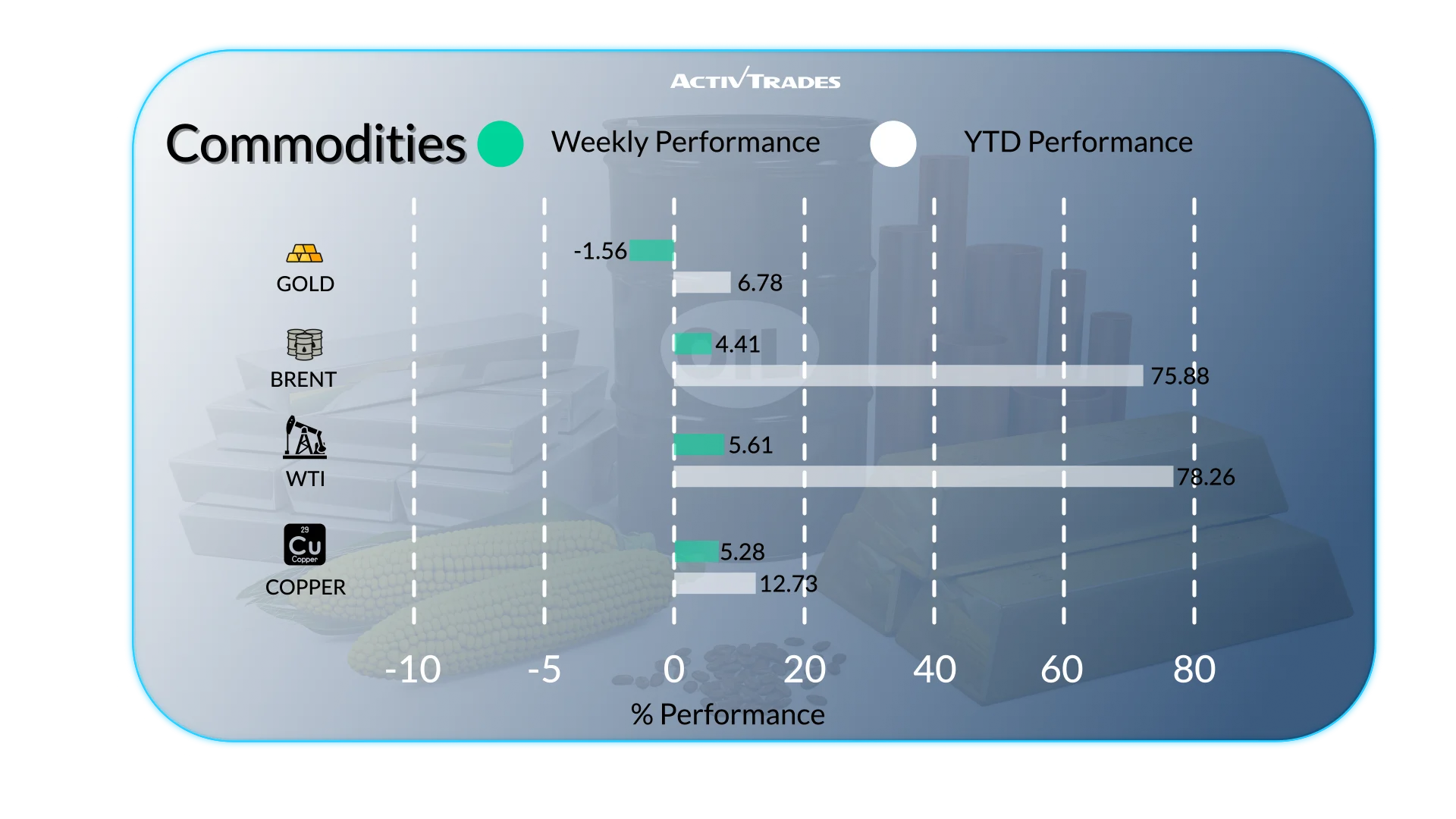

Commodities

- Oats prices are up more than 11%.

- WTI prices are up more than 7.50%.

- US Wheat prices are up more than 6%.

- Natural Gas and Brent prices are up more than 5.5%.

- Orange Juice prices are up more than 4%.

- Palladium prices are down more than 4%.

- Gold prices are down more than 3%.

- Platinum prices are down more than 2%.

Indices

- The KOSPI index is up more than 2.4%.

- The S&P500 index is up more than 1.6%.

- The Bovespa index is down more than 4.9%.

- The CAC40 index is down more than 2.8%.

- The Japan 225 and the Bist 100 index are down more than 2%.

Shares

Tops

- Akamai Technologies: +34.05%

- Braskem: +29.67%

- Cisco Systems: +25.58%

- Palo Alto Networks: +24.87%

- Coherent: +23.14%

- Humana: +22.61%

- Micron Technology: +19.42%

- CrowdStrike: +19.31%

- Fortinet: +15.78%

- NVIDIA: +13.88%

- British American Tabacco: +13.81%

- Infineon Technologies: +12.59%

- STMicroelectronics: +12.11%

- Compass: +11.26%

Flops

- Mettler-Toledo International: -21.89%

- 3i Group: -21.46%

- Rheinmetall: -19.61%

- Vivara Participaoes: -18.93%

- Zoetis: -16.75%

- Charles River Laboratories: -15.94%

- Azzas 2154: -15.51%

- DoorDash: -15.47%

- Trade Desk: -15.24%

- Constellation Energy: -14.78%

- Thomson Reuters: -14.34%

- Badcock International: -13.41%

- MercadoLibre: -13.15%

Important Events to Follow

Monday 18 May

- 02:00 AM - Chinese - Industrial Production YoY (April)

- Previous: 5.7%

- Forecast: 5.5%

- 02:00 AM - Chinese - Retail Sales YoY (April)

- Previous: 1.7%

- Forecast: 2.2%

- 11:50 PM - Japanese - GDP Growth Rate QoQ Prel (Q1)

- Previous: 0.3%

- Forecast: 0.1%

Tuesday 19 May

- 12:30 AM - Australian - Westpac Consumer Confidence Change (May)

- Previous: -12.5%

- Forecast: -1.1%

- 01:30 AM - Australian - RBA Meetings Minutes

- 06:00 AM - UK - Unemployment Rate (March)

- Previous: 4.9%

- Forecast: 5.1%

- 12:30 PM - Canadian - Inflation Rate YoY (April)

- Previous: 2.4%

- Forecast: 3.0%

Wednesday 20 May

- 06:00 AM - UK - Inflation Rate YoY (April)

- Previous: 3.3%

- Forecast: 2.6%

- 06:00 PM - American - FOMC Minutes

- 11:00 PM - Australian - S&P Global Manufacturing PMI Flash (May)

- Previous: 51.3

- Forecast: 50.6

- 11:00 PM - Australian - S&P Global Services PMI Flash (May)

- Previous: 50.7

- Forecast: 49.9

- 11:50 PM - Japanese - Balance of Trade (April)

- Previous: ¥667B

- Forecast: ¥-150.0B

Thursday 21 May

- 12:30 AM - Japanese - S&P Global Manufacturing PMI Flash (May)

- Previous: 55.1

- Forecast: 54

- 12:30 AM - Japanese - S&P Global Services PMI Flash (May)

- Previous: 51.0

- Forecast: 50.7

- 07:15 AM - French - S&P Global Composite PMI Flash (May)

- Previous: 47.6

- Forecast: 47.1

- 07:15 AM - French - S&P Global Manufacturing PMI Flash (May)

- Previous: 52.8

- Forecast: 52.7

- 07:15 AM - French - S&P Global Services PMI Flash (May)

- Previous: 46.5

- Forecast: 46

- 07:30 AM - German - S&P Global Manufacturing PMI Flash (May)

- Previous: 51.4

- Forecast: 51.6

- 07:30 AM - German - S&P Global Composite PMI Flash (May)

- Previous: 48.4

- Forecast: 48

- 07:30 AM - German - S&P Global Services PMI Flash (May)

- Previous: 46.9

- Forecast: 46.2

- 08:00 AM - European - S&P Global Composite PMI Flash (May)

- Previous: 48.8

- Forecast: 47.5

- 08:00 AM - European - S&P Global Manufacturing PMI Flash (May)

- Previous: 52.2

- Forecast: 52.5

- 08:00 AM - European - S&P Global Services PMI Flash (May)

- Previous: 47.6

- Forecast: 47

- 08:30 AM - UK - S&P Global Manufacturing PMI Flash (May)

- Previous: 53.7

- Forecast: 51.2

- 08:30 AM - UK - S&P Global Services PMI Flash (May)

- Previous: 52.7

- Forecast: 51.7

- 12:30 PM - American - Building Permits Prel (April)

- Previous: 1.363M

- Forecast: 1.35M

- 12:30 PM - American - Housing Starts (April)

- Previous: 1.502M

- Forecast: 1.45M

- 01:45 PM - American - S&P Global Composite PMI Flash (May)

- Previous: 51.7

- Forecast: 51.5

- 01:45 PM - American - S&P Global Manufacturing PMI Flash (May)

- Previous: 54.5

- Forecast: 53

- 01:45 PM - American - S&P Global Services PMI Flash (May)

- Previous: 51.0

- Forecast: 51.1

- 11:30 PM - Japanese - Inflation Rate YoY (April)

- Previous: 1.5%

- Forecast: 1.8%

Friday 22 May

- 06:00 AM - German - GfK Consumer Confidence (June)

- Previous: -33.3

- Forecast: -34

- 06:00 AM - UK - Retail Sales MoM (April)

- Previous: 0.7%

- Forecast: 0.3%

- 08:00 AM - German - Ifo Business Climate (May)

- Previous: 84.4

- Forecast: 82

Major Earnings Reports to Watch

Monday 18 May

- BAIDU

Tuesday 19 May

- HOME DEPOT

Wednesday 20 May

- Target

- Lowe'S Cos

- Ubisoft Entertainment

- EXPERIAN

Thursday 21 May

- Zoom

- WALMART

- Swiss Life

Friday 22 May

- Compagnie Financiere Richemont

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of May 15, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.